Weekly Snack #5

New Equity Idea Generation, Twitter Posts, and General Reasearch of the Week

Welcome to Weekly Snacks! This newsletter is home to a weekly compilation of new investment ideas, Twitter posts/threads, and general research to help all investors generate ideas that they may have otherwise not been exposed to.

If you find our posts helpful, please click the subscribe button below (it’s free), and if you yourself have an idea you’d like to share with us to possibly be featured, comment below.

Investment Pitches

TL;DR:

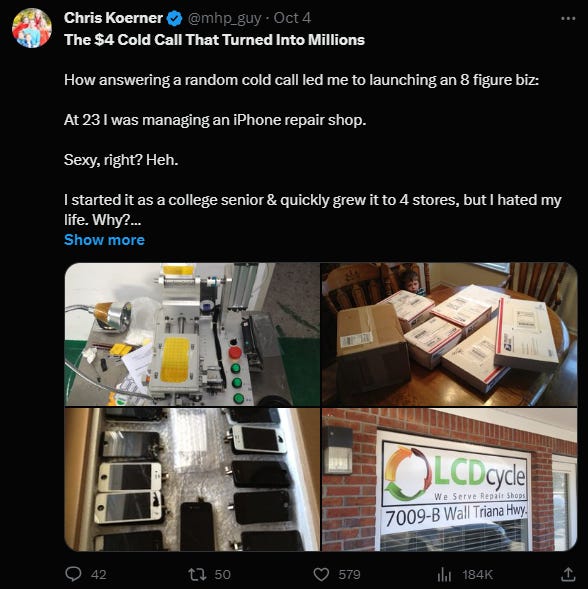

InPost (AMS:INPST) is an interesting company because if you live in a major metropolitan city, you’ve seen those lockers used to drop off/return packages. InPost is one of those companies but based in Poland and is said that 60% of the population lives within 7 minutes of once of these automaed parcel machines (APMs). Jake argues that the company is underrated because while the company is expanding internationally (UK & France), the company is not draining cash and InPost continues to generate upsized FCF. This increases the liklihood for an aysmmetric return into the future.

TL;DR:

Dollar General (DG) has been on the minds of lots of investors and Siyu Li is an investor I follow for his interesting takes on companies. He posted his thoughts on Dollar General (DG) breaking down unit level economics, limitations of the whole business model and what that means going forward. Providing his own DCF, you’d be surprised where he lands based on projections to 2030. if you’re interested in the name, take a quick look at his thoughts before making a decision.

TL;DR:

Fairway Research posted their thoughts on Sleep Country (ZZZ), a Canadian mattress retailer. For anyone that’s been following the American mattress companies over the last decade, they haven’t been performing well in the slightest. However, the author argues that the strategy of ZZZ is proving to be a good one for a number of reasons. The tortoiuse and the hare type of situation has allowed the comapny to expand strategically, buy up competitors at pennies on the dollar, and realize that brick and mortar customer service and superior delivery experience is really helping them out in this overly saturated market. With a supposed 30% upside return, I would highly encourage you reading this deep dive.

TL;DR:

Waste Connections (WCN) is a waste dispoal company in the US that offers investors a high barrier to entry against competitors, and more of a defensive play into uncertain times. The author believes that the company’s historic decisions of capital allocation, ability to leverage its resilient business model and consistent slower growth trajectory of the overall industry are quite attractive. For a company that deals in waste, FCF as a percent of sales is industry leading at 16% and the author suggests based on their own model that the company could deliver a 14% IRR by YE’26.

TL;DR:

Synaptics (SYNA) is an interesting company because they operate in the world of physical tech by providing mixed signal semiconductor solutions to everyday devices like phones, computers, and other IoT devices. The author suggests that while the overall semiconductor industry is normalizing, managements execution has been greatly tied to long-term incentives partially based on tenure and KPIs of the company. While SBC is abundant at SYNA, the company still has a roadmap for continued growth and profitabilty which the author believes could deliver double-digit returns over the next 5 years.

Tweets of the Week

General Research

Appreciate you taking the time to read Weekly Snacks. I hope you have found at least some of these links to be interesting enough to dive into yourself.

If you haven’t already, consider hitting the subscribe button below and sharing this Substack with someone you know.

Until next week,

Paul Cerro