Weekly Snack #35

New Investment Pitches, General Research, and Tweets of the Week

Welcome to Weekly Snacks! This newsletter is home to a weekly compilation of new investment ideas, Twitter posts/threads, general research, and podcasts to help all investors generate ideas that they may have otherwise not been exposed to.

If you find our posts helpful, please click the subscribe button below (it’s free), and if you have an idea you’d like to share with us to possibly be featured, comment below.

Investment Pitches

TL;DR:

Author Bill Huang shared their thoughts on Watches of Switzerland Group (WOSG) in what they highlight as a market misunderstanding of the future of watch retailing. Currently, the market is hitting WOSG because of assumptions that Rolex might be selling their goods via DTC, essentially hitting WOSG retail arm since 55% of WOSG’s sales is directly related to Rolex. The author also points to a recent deterioration of the stock related to a broader luxury slowdown which we’ve seen recently in other names. Bill thinks it’s highly unlikely that Rolex will start to sell via DTC and that the licensing part of the Rolex business is what protects WOSG from competitors.

TL;DR:

An interesting special situation is on K2A Knaust & Andersson Fastigheter AB (K2A Pref) preferred shares specifically. Earlier in the year, the company suspended the dividend due to liquidity constraints and the stock quickly sold off by 50%. However, preferred shares still need to have their unpaid dividends paid in the future alongside a 12% penalty on unpaid amounts. Given that the company has been able to sell a share of a building for $600 million SEK, the company is in a much better financial position to pay its future bond obligations which means that the future for the preferreds could be advantageous now than it was just a few months ago. Antartic Circle thinks investors can benefit from a 13.89% yield plus potential share price appreciation, with minimal foreseeable risk.

TL;DR:

Last week, Bleeker Street Research posted a short report on Dave Inc (DAVE) in what they believe is a predatory lender disguised as a consumer-friendly fintech. The author highlights that DAVE’s “tipping” feature has allowed it to essentially capture loan-shark level APRs though customers have been slowly wising up to this scheme. Tipping is a large part of the business (22% of ‘23 sales and contributed $42M in contribution profits) and because customers are tipping less, Bleeker suggests that the actual earnings of DAVE would swing to massive operating losses. An interesting read for anyone in that space.

TL;DR:

I actually posted about Red Cat Holdings (RCAT) back in Weekly Snacks 33 but at the time I hadn’t done my own due diligence on it. After I did, I realized that a lot of the authors assumptions were incorrect and misleading. I published my thoughts on the event-driven trade, the math behind the U.S. Army contract that the company is a finalist for any why I believe that the upside of 200% if they win might just be the tip of the iceberg.

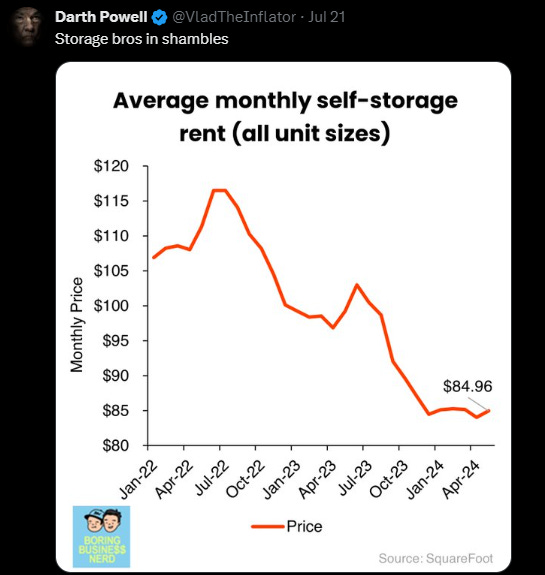

Tweets of the Week

General Research

Podcasts

Appreciate you taking the time to read Weekly Snacks. I hope you have found at least some of these links to be interesting enough to dive into yourself.

If you haven’t already, consider hitting the subscribe button below and sharing this Substack with someone you know.

Until next week,

Paul Cerro