Weekly Snack #33

New Investment Pitches, General Research, and Tweets of the Week

Welcome to Weekly Snacks! This newsletter is home to a weekly compilation of new investment ideas, Twitter posts/threads, general research, and podcasts to help all investors generate ideas that they may have otherwise not been exposed to.

If you find our posts helpful, please click the subscribe button below (it’s free), and if you have an idea you’d like to share with us to possibly be featured, comment below.

Investment Pitches

TL;DR:

First off, I love everything about this pitch. I actually might buy it myself. Multibagger Monitor shared his thoughts on an event driven trade for Red Cat Holdings (RCAT). Red Cat is in the final 2 for a DoD contract for defense drones that could total multiples of what the current market cap is. The author goes into detail what makes the contract so interesting, how the company stacks up against the other competitor, and what the potential upside could be should they win. The decision is likely to be announced in September.

TL;DR:

Next pitch comes from DF Research who is short Willscot Home Mini (WSC). Kieth goes into detail that the company’s favorable capex spending relative to its peers is actually not because of efficiency but rather significant underinvestment in its aging fleet of mobile homes. Because of this underinvestment, the company is sitting on assets that are old, decrepit and otherwise “unrentable”. Additionally, the low utilization rates relative to peers seems to hide in the shadows of optimistic forward guidance and the abnormally large share buybacks. Kieth thinks it has plenty of more room to fall and based on his evidence, I would agree.

TL;DR:

Eagle Point Capital shared their thoughts on Advance Auto Parts (AAP) potentially being the time for their turnaround moment. For years, the company has dramatically underperformed its peers ORLY and AZO. Eagle goes into what management has highlighted as value creation priorities that could help the company start righting the ship. With a depressed FCF margin, even correcting this by just a few hundred basis points could really add significant tailwinds for reinvestment should the company be able to execute. But I love the way he leaves it off, “The problem is, the same opportunity exists today that existed in 2015.”

TL;DR:

Given the recent price action, I wanted to highlight my pitch on GEN Restaurant Group (GENK). It’s a very simple Korean BBQ chain that is rapidly expanding outside its core California stomping grounds. The unit prospects for the company are not outrageous either and with AUV and comprable margins similar to other peers, the base effects of unit growth can really supercharge this company’s returns. While it’s not the next Chipotle, that doesn’t mean that it can’t become a multi-bagger in the future.

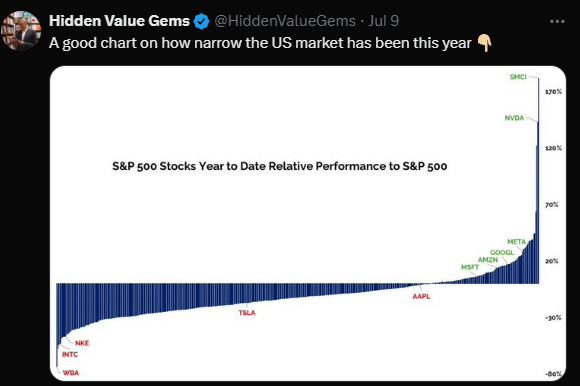

Tweets of the Week

General Research

Podcasts & Interviews

Appreciate you taking the time to read Weekly Snacks. I hope you have found at least some of these links to be interesting enough to dive into yourself.

If you haven’t already, consider hitting the subscribe button below and sharing this Substack with someone you know.

Until next week,

Paul Cerro