Weekly Snack #34

New Investment Pitches, General Research, and Tweets of the Week

Welcome to Weekly Snacks! This newsletter is home to a weekly compilation of new investment ideas, Twitter posts/threads, general research, and podcasts to help all investors generate ideas that they may have otherwise not been exposed to.

If you find our posts helpful, please click the subscribe button below (it’s free), and if you have an idea you’d like to share with us to possibly be featured, comment below.

Investment Pitches

TL;DR:

Brainless Investing wrote a piece on Atkore International (ATKR), who is a manufacturer of infrastructure porducts. ATKR has had an impressive run over the last 10 years, growing revenue at a 9% CAGR and EPS of 21%. While mny investors might argue that the future is still very bright, the author argues that it’s too difficult to determine if there’s still juice left to squeeze. None of management have bought shares in the last year and in order to reach a 15% annual IRR, the company needs to generate at least 9.5% CAGR in FCF growth which is very optimistic. If the market over-reacts, the author thinks it would be worth revisitng.

TL;DR:

The Mikro Cap wrote a very long but very thorough report on Alico (ALCO), Florida’s largest orange producer. David goes into detail what helped lead to the companiy’s decline but what is now arguably helping it turnaround. He goes in-depth about market share related to land, diseases that have been killing crops and lowering yields, etc. Like I said, it is a long pitch but one of the better one’s that covers a single name. If you’re interested in a turnaround that has some acceleration, I’d take a look at this one.

TL;DR:

Grizzly Research put out a short report on Pinterest (PINS) claiming that the company is seeing its user base leave in droves due to poor changes in user experience, ad spams, while also engaging in fraudulent click-farms to secure KPIs. Grizzly dives deep into what they believe are sings that KPIs are being manipulated and that web traffic is declining rapidly all while the company is pushing hard into low-income markets. They label this stage of their business as a “death spiral” with an inevitable price range of $5 - $16/share.

TL;DR:

I wrote my thoughts on Mama’s Creations (MAMA) and the stock has done incredibly well since. There isn’t rocket science that goes into this name nor is it even remotely a sexy business. The thesis to this name is that the company has successfully executed a turnaround and continuing under the helm of the current CEO, more of the same can be expected. The market is very fragmented which leaves room for lots of M&A in the future to help drive growth toward its $1 billion revenue target. As fas a names go that have plenty of upside over the long-term without needing to swallow tons of volatility, MAMA is a name you should be interested in.

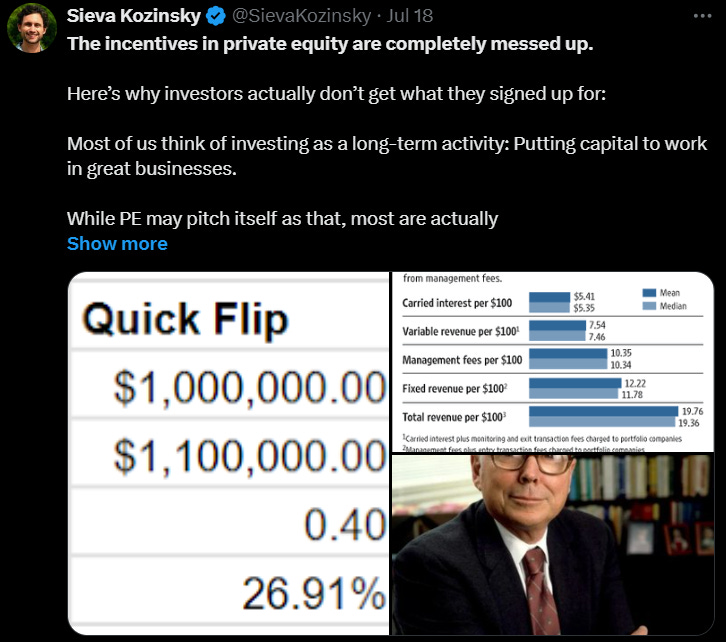

Tweets of the Week

General Research

Appreciate you taking the time to read Weekly Snacks. I hope you have found at least some of these links to be interesting enough to dive into yourself.

If you haven’t already, consider hitting the subscribe button below and sharing this Substack with someone you know.

Until next week,

Paul Cerro