Weekly Snack #3

New Equity Idea Generation, Twitter Posts, and General Reasearch of the Week

Welcome to Weekly Snacks! This newsletter is home to a weekly compilation of new investment ideas, Twitter posts/threads, and general research to help all investors generate ideas that they may have otherwise not been exposed to.

If you find our posts helpful, please click the subscribe button below (it’s free), and if you yourself have an idea you’d like to share with us to possibly be featured, comment below.

Investment Pitches

TL;DR:

This is a rather interesting one because it’s not one that I’ve personally ever read anywhere. The author talks about a notable HF manager on Twitter named Kuppy (I follow him) and how he created an investment vehicle in Mongolia (Mongolia Growth Group) to capitalize on one of the rising asian countries. Long story short, changes in the country led investments to be not as easy going. However, the fund (MCG) is an interesting play because it’s trading under NAV and there are a few ways for investors to make money while taking some exposure. Have a read above, it’s not long.

TL;DR:

The author suggests that Chewy (CHWY) is a fundamentally good business but is dealing with macroeconomic pressures and changes in consumer perception are affecting the dog industry. The company has greatly expanded it’s margins and growth since going public but the market is punishing it based on a dissapointing full-year outlook. The company is also facing churn risks, stock-based compensation payouts, and lack of operating leverage. This is one for if you believe the market is pricing it appropriately.

TL;DR:

Fair warning, this is a very long read but really hits home all the points when talking about Adyen (ADYEY) and Paypal (PYPL). The author goes into great detail about the companies financial health, their ability to generate FCF and what growth means for each company. Granted, PYPL has slowed down significantly while ADYEY still has double digit growth but the market has clearly punished it. Author makes a comment about how investors think PYPL could be META 2022 but highlights why that’s not the case. ADYEY has substantial room for growth but admits that we’re still in a highly competitive environment.

TL;DR:

The author talks about Sankyo (DSNKY), a Tokyo listed maker of gaming machines. While Japan has gotten quite a bad wrap over the years, the author points out that the company has been consistenly profitbable over the last 20 years, each year. The market cap is made up of ~70% cash and ST investments while trading at a measly 1.5x EV/EBITDA. In the pitch, while industry forces seem to be working against the broader industry, the author highlights what Sankyo is doing differently to moderinize itself and boost growth again for the new gaming age.

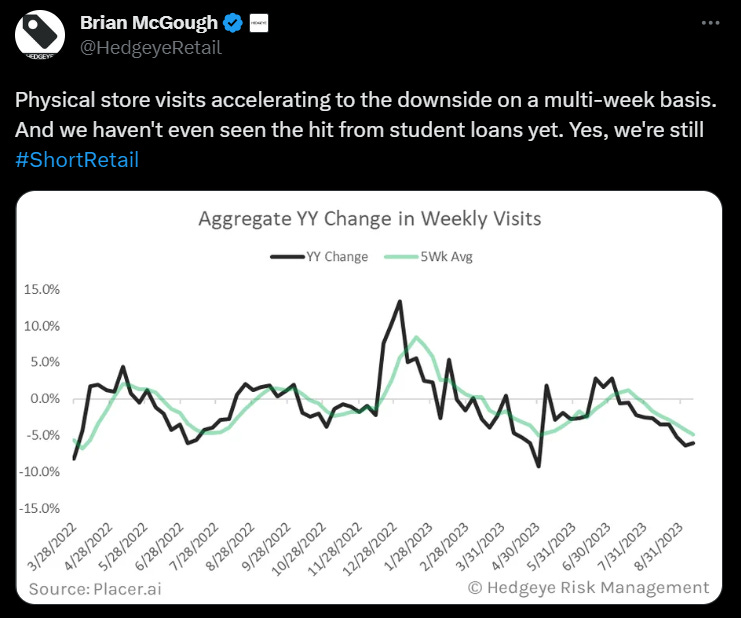

Tweets of the Week

General Research

Appreciate you taking the time to read Weekly Snacks. I hope you have found at least some of these links to be interesting enough to dive into yourself.

If you haven’t already, consider hitting the subscribe button below and sharing this Substack with someone you know.

Until next week,

Paul Cerro