Weekly Snack #28

An interesting deSPAC with organs, UK greeting cards and Korean BBQ?

Welcome to Weekly Snacks! This newsletter is home to a weekly compilation of new investment ideas, Twitter posts/threads, general research, and podcasts to help all investors generate ideas that they may have otherwise not been exposed to.

If you find our posts helpful, please click the subscribe button below (it’s free), and if you have an idea you’d like to share with us to possibly be featured, comment below.

Investment Pitches

TL;DR:

I really enjoyed this pitch from The Last Bear Standing on Blade Air Mobility (BLDE). He literally starts off his pitch with “no one seems to think this is a good company” probably because it’s a deSPAC that nosedived since going public. The value here is that the Blade that we all knew from inception was transporting rich people (or wannabe rich people) via helicopters and planes to top destinations. However, the company expanded into medical transportation and has really taken off since then, accounting for a majority of its revenue in 2023. The asset-light nature (10% of aircraft is leased) of this business, opportunity in the medical transport space, optimization of short form travel can help it become profitable as as soon as this year. It’s an interesting play and the author did a great job breaking down the transition, market opportunity, and the financials.

TL;DR:

This one is interesting because it deals with the very boring business of greeting cards. David Katunarić over at Mikro Kap posted his updated thoughts on Card Factory (CARD.L), in what he describes as, “Cardonomics”. Card Factory is a UK based greeting card company that has over 1,000 locations and control ~30% of the market. He makes the case that the company is best positioned to beat out its rivals through vertical integration, ability to have favorable lease-terms on their locations, a dividend suspension that is expired, its ability to gorw new stores at an attracive ROIC. It sounds so dumb when you’re reading a pitch about greeting cards but I really enjoyed reading this one by David where he hints at possibly achieving a +20% CAGR.

TL;DR:

First time mention from Brandon over at Macro Ops and his thoughts on GEN Restaurant (GENK), is a Korean BBQ-themed all-you-can-eat restaurant. Brandon argues that the company can do well because guests can cook their food which reduces the need for kitchen space so more tables can be added and thus, improving sales per square foot. This also has an effect on store level margins because GENK doesn’t need to hire chefs and outfit an expensive kitchen. Store expansion (37 → 250+) and 40% store returns are just the few attractive pieces about this pitch. Brandon believes this could be a 5x-bagger in the future.

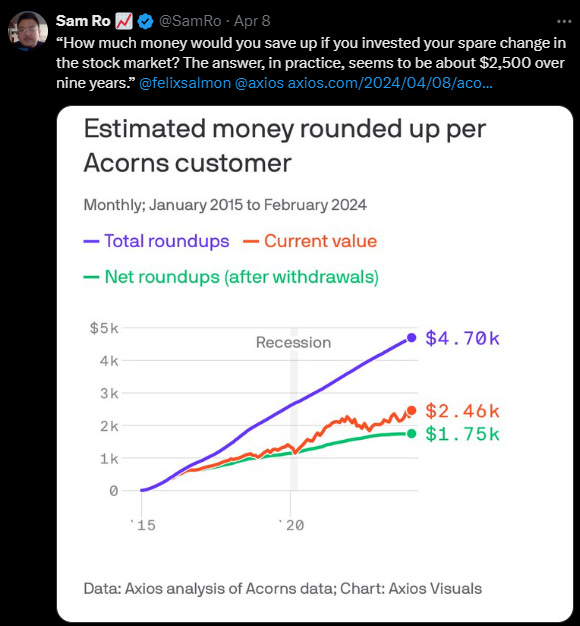

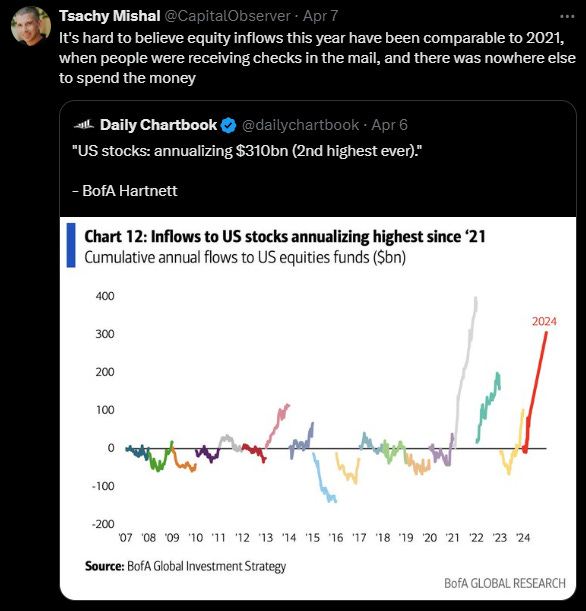

Tweets of the Week

General Research

Podcasts & Interviews

Appreciate you taking the time to read Weekly Snacks. I hope you have found at least some of these links to be interesting enough to dive into yourself.

If you haven’t already, consider hitting the subscribe button below and sharing this Substack with someone you know.

Until next week,

Paul Cerro

Thanks for highlighting, Paul!