Weekly Snack #23

A very interesting special situation, an undervalued frac sand company and filtration systems yielding a good return?

Welcome to Weekly Snacks! This newsletter is home to a weekly compilation of new investment ideas, Twitter posts/threads, general research, and podcasts to help all investors generate ideas that they may have otherwise not been exposed to.

If you find our posts helpful, please click the subscribe button below (it’s free), and if you yourself have an idea you’d like to share with us to possibly be featured, comment below.

Investment Pitches

TL;DR:

First share of the week comes from Under-Followed-Stocks and his pitch on Civitanavi Systems SpA (CNS.MI), a player in the inertial navigation systems industry. The author believes that the company’s products, which is used for space launch systems, military vehicles, and in the oil and gas industry, could bring investors rich returns. The company is founder-led with high ownership interest, and has been able to grow revenue at a 63% CAGR from 2012 - 2022. Trading ~12x EBIT, projected growth in the company and margins makes this not an expensive play on the future.

TL;DR:

Eagle Point Capital posted a really interesting special situation on Cummins CMI 0.00%↑ and Atmus Filtration Technologies ATMU 0.00%↑. The context is that Cummins recently settled litigation with the state of California and DOJ where their settlement of $2 billion hit Q4 earnings and consequently, the company is now looking to buy back shares as they believe their share price is undervalued. The play here is that the company is looking to buy back shares (via tender offer) and investors will recieve $107.53 of Atmus stock for every $100 in CMI tenderd. There are risks here depending on odd-lots and upper limits as part of the exchange. If you’re early enough, you might be able to receive a risk-free 7.5% return in a matter of days.

TL;DR:

Stonks’s Substack wrote a post on Smart Sand SND 0.00%↑, one of the largest suppliers of high quality frac sand. The company was hit hard during the bust of over-fracking supply and COVID. Given their balance sheet at the time, the company was lucky enough to buy a lot of their bankrupt competitors assets on the cheap when things started to rebound. SND currently trades at ~50% of liquidation value and 30% of book value and the author believes that this is a low-risk investment with practically no debt. Given the recent track record of increased sales + guidance, he’s optimistic enough to make this 25% of his portfolio.

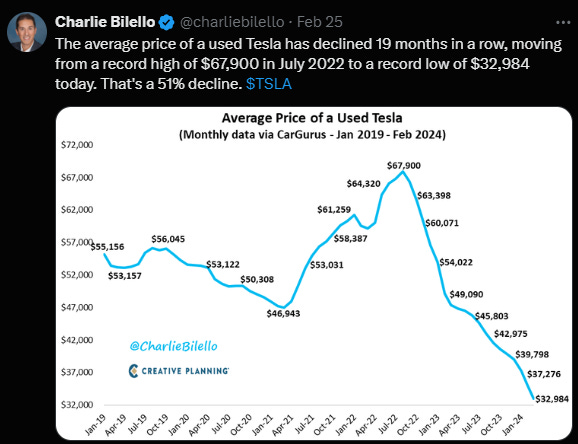

Tweets of the Week

General Research

Podcasts & Interviews

Appreciate you taking the time to read Weekly Snacks. I hope you have found at least some of these links to be interesting enough to dive into yourself.

If you haven’t already, consider hitting the subscribe button below and sharing this Substack with someone you know.

Until next week,

Paul Cerro