Weekly Snack #12

New Equity Idea Generation, Twitter Posts, and General Reasearch of the Week

Welcome to Weekly Snacks! This newsletter is home to a weekly compilation of new investment ideas, Twitter posts/threads, and general research to help all investors generate ideas that they may have otherwise not been exposed to.

If you find our posts helpful, please click the subscribe button below (it’s free), and if you yourself have an idea you’d like to share with us to possibly be featured, comment below.

Investment Pitches

TL;DR:

An interesting take this week from author hourglass on Dentalcorp (DNTL.TO), a dental practice serial acquirer. The author believes that the recent decline in the stock price is attributed to a leveraged balance sheet and selling pressure from investors who were looking to make a buck. Hourglass makes note of slowing growth and a decline in EBITDA, but that’s mainly driven by the nature of the enviroment that we’re in. Should the company be able to bounce-back in the next few years, given that dentistry is recession-resistant (not proof), a multiple re-rating on the stock could offer investors an over 100% return by then.

TL;DR:

A super short read but the author, Emerging Value, talks about 4 cheap energy stocks Repsol (BME.REP), OMV (OMV.VI), Orlen (PKN.WA), and Vermilion Energy (VET). While a short read, he basically creates a brief breakdown, opportunities and risk profile for each. If you’re interested in the energy space and want exposure besides US energy related companies, have a read.

TL;DR:

A micro cap company, one that Cedar Grove Capital Management is invested in, was published by author Kairos research. Mama’s Creations (MAMA) is a pre-packaged italian food company that operates across the US. This company has been featured in Value Investors Club (VIC) before and the author breaks down the company’s transition that has captured the eyes of value investors. Without huge margin expansion, even though they could, Kairos calculations over the next 5 years could yield investors anywhere between 37% - 187% dependent on topline growth and multiple expansion. Have a read, it’s a no-name company that might catch your eye as it did mine a few months ago.

TL;DR:

Another interesting idea from Ironside Research is about SS&C Technologies (SSNC) who specializes in financial services operations. The company signs up customer contracts in the financial services space between 1 - 5 years and removes the headaches of running the business backend so that these funds can worry about the important part. Making money. Ironside believes that much of the turmoil has to do with interest rates as the company is primarily dependent on acquisitions for growth. Given interest rates are high right now, that could change in the near future. Based on his reverse DCF, the implied value could very well result in considerable upside given he believes the punishment is overdone. An interesting read and quite literally a company I’ve never head of.

TL;DR:

Sharing my thoughts on the Tapestry (TPR) and Capri Holdings (CPRI) M&A deal that was announced in August. The spread between the two premium retailers has widened over the last month after the FTC sent over a second request for more information. In the post, I go over the points associated with why investors may or may not believe the deal will close next year. Despite some calls for anti-trust and financing issues, I believe that the deal lacks concern for governments to not allow this to go through. Have a read and let me know if you think otherwise.

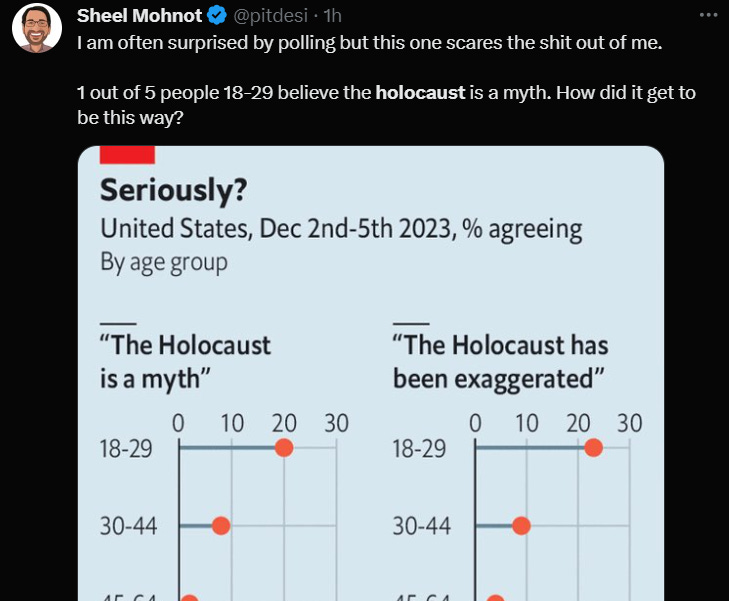

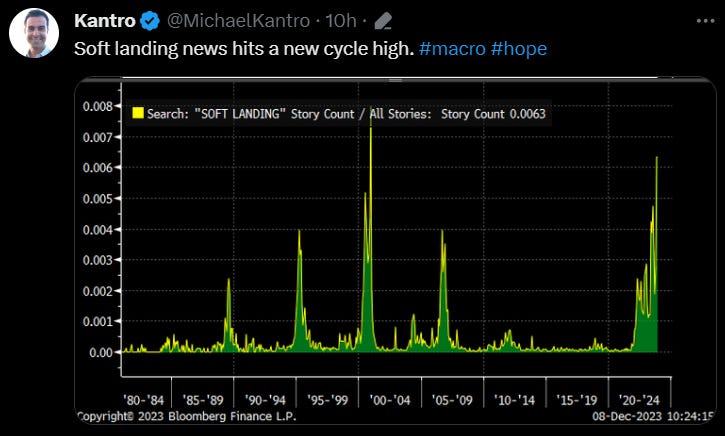

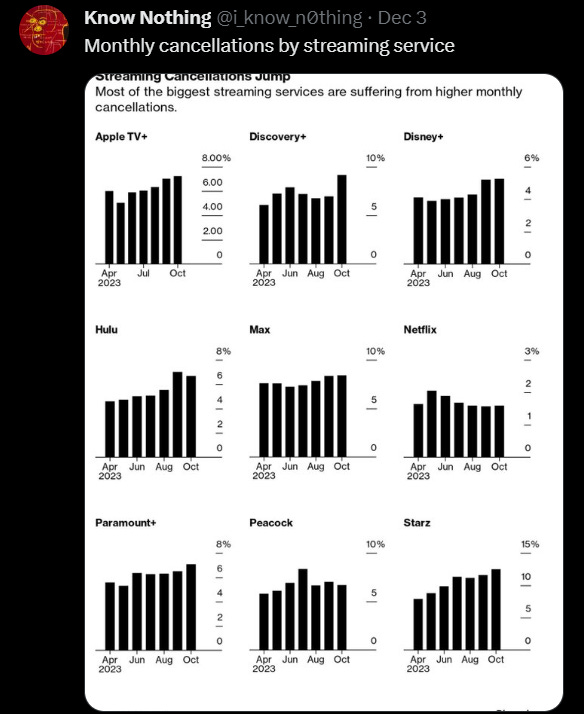

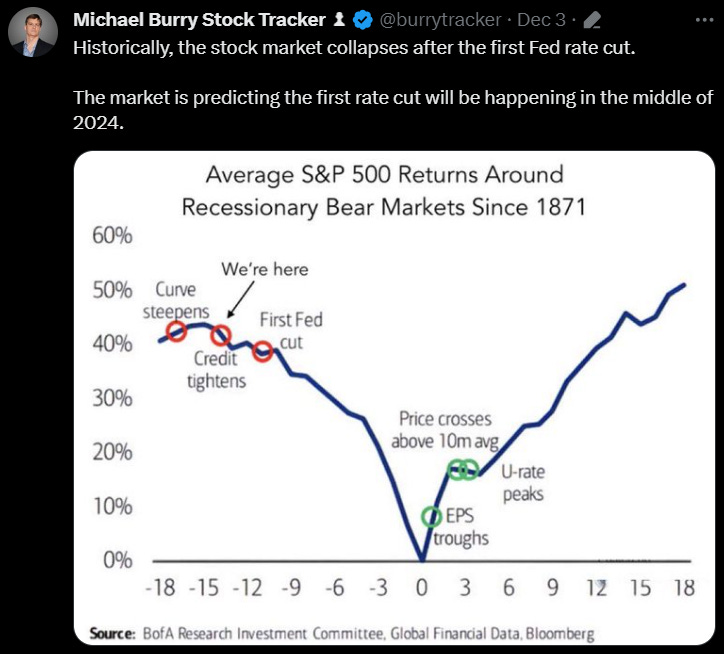

Tweets of the Week

General Research

Appreciate you taking the time to read Weekly Snacks. I hope you have found at least some of these links to be interesting enough to dive into yourself.

If you haven’t already, consider hitting the subscribe button below and sharing this Substack with someone you know.

Until next week,

Paul Cerro

Thanks for mentioning the dentalcorp article! Appreciate it